Gold, real-estate or business: How do households intend to save?

How has the Covid-19 pandemic affected personal (household) savings? There is a trade-off between current liquidity and locking money away in assets. We need liquidity to take care of immediate financial needs. We also save (invest) in financial or other assets as protection against future shocks or for longer term gains, e.g. invest in gold, real estate or in a fixed deposit or mutual fund. Savings are higher when people feel financially secure in the present. When incomes take a hit, for instance, as a result of job losses due to the pandemic, people can run down their savings.

According to RBI, India had a household financial savings rate of 10.4 percent in the July-September 2020 quarter. This was a sharp decline from 21 percent in the previous quarter (April to June). The savings rate declined further to 8.2 percent in the October-December 2020 quarter. RBI figures show that the Covid-19 pandemic has led to a decline in financial assets such as bank deposits, pension money, life insurance funds and currency holdings.

In our previous bulletins, we discussed how the pandemic has negatively affected employment, including manufacturing employment, household incomes and wages, and household expenses. In this CEDA-CMIE bulletin, we focus on intention to save. Intention to save is different from actual savings as it reflects people’s mood or sentiment about the immediate future. Intentions might not match actual actions. However, intention to save is a good barometer of economic anxiety: when intention to save (or actual savings) take a hit, it indicates that people are unwilling to lock away liquidity despite the advantage of future use or gain.

Like we did in our earlier bulletins, we take a longer look at how intention to save has changed from January 2017 to April 2021, instead of zooming in narrowly around the pandemic.

CMIE provides us the percentage of surveyed households who intend to save in a particular instrument (or avenue) for example gold or real estate or fixed deposits, in the next 120 days from the date of survey. The CMIE data provides these percentages for all households as well as broken down by slabs of annual household incomes.

This helps us understand how intention to save in specific instruments varies by the income profile of savers. For example, in the July-September 2020 quarter, 1.4 percent respondents expressed an intention to invest in gold in the next 120 days. But if we take a look at income groups, we find that among the households with an annual income of more than INR 1 million per annum, this number rises to 3.06 percent. This is expected as richer households are more likely to save in gold (i.e. buy gold).

CMIE data collects information about 13 savings avenues. In this bulletin we will focus on three of those, namely: gold, business, and real estate. In the next CEDA-CMIE bulletin, we will focus on the intention to save in fixed deposits, life insurance, post office savings, provident fund, mutual funds, listed shares, NSC, and Krishi Vikas Patra. Since the CMIE data is nationally representative on a quarterly basis, we look at year on year changes at a quarterly level (from January to March 2017 and so on).

When we look at data for these three categories, we observe a broad decline in intention to save in these instruments since October-December 2019. In Figure 1, we take a closer look at gold across various income groups.

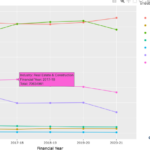

Figure 1, depicts the intention to save in gold over the next 120 days for all income groups and all quarters starting from Jan-Mar 2017. It also shows us the average quarterly prices for gold in this period.

Figure 1

Figure 1 shows that the intention to save in gold hit a peak in July-September 2018 (for all income groups combined). We see a consistent decline in gold’s popularity amongst savers since December 2019. The highest intention to save in gold is seen in the top income bracket.

It is important to note that high net worth individuals are under-represented in all household surveys, everywhere in the world. This is because it is very difficult, if not impossible, to get the super-rich to answer survey questions. The CMIE data has some representation from households earning more than INR 1 million per annum, which gives a glimpse into their savings intentions.

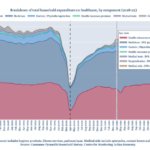

In Figure 2, we plot the intention to invest in real estate by income groups.

Figure 2

We see a decline in intention to save in real estate among all income groups since April-June 2019. For all income groups combined, real estate hit the peak interest in October-December 2018 with 6.62 percent respondents expressing an intention to save in it over the next 120 days. Through most of the period for which we analyzed the data, real estate remained more popular among households with annual incomes between INR 2-5 lakh per annum. We also observe a revival of interest in real estate for the higher income groups (INR 5 lakh to 1 million per annum, and more than INR 1 million per annum) since January-March 2021, but a dip in April 2021.

In Figure 3, we look at “business” as an investment avenue for respondents. We see a broad increase in business’ popularity since January-March 2017 (except a minor dip in July-September 2020). This may be explained by the fact that business investment is also an income generation activity. With incomes hit, there may have been added incentive to invest in businesses to ensure that income flow is less affected. Moreover, with Covid-19, new opportunities to earn came into existence (e.g. home deliveries, mask-making etc) which may explain why investment in businesses doesn’t exhibit the trends other saving instruments show.

Not surprisingly, the richest group of households (income greater than INR 1 million) show the highest propensity to invest in business. There was an increase in intention to save in business in the first quarter of 2021, but in April 2021, this took a strong hit because of the devastation unleashed by the strong second wave of coronavirus hurting Indian economic activity.

Figure 3

As is the case with several other economic aggregates like employment or output, the downward trend in intention to save started before the Covid-19 pandemic, but has worsened with the pandemic.

This reflects current economic uncertainty; additionally, it shows a vicious cycle. Household savings that get channelled into real estate or business can provide a boost to economic activity and help the economy to recover. But if people are hesitant to lock their money for longer periods because of the precarity of the current economic situation, that makes the prospects of future recovery that much weaker. The only way to break this vicious cycle is for the government to impart a strong fiscal stimulus, put money in the hands of households as we have outlined earlier which will help to alleviate economic anxiety in the present.

If you wish to republish this article or use an extract or chart, please read CEDA’s republishing guidelines.

Related posts

CEDA-CMIE Bulletin: How households intend to save – Part 2

CEDA-CMIE Bulletin: How households intend to save – Part 2

What data has been telling us: The job crisis is real

What data has been telling us: The job crisis is real

How much do Indian households spend on healthcare every month?

How much do Indian households spend on healthcare every month?

Covid-19 and lockdown: Impact on household and individual wage income

Covid-19 and lockdown: Impact on household and individual wage income

Covid-19 and lockdown: How household expenses bore the brunt

Covid-19 and lockdown: How household expenses bore the brunt