CEDA-CMIE Bulletin: How households intend to save – Part 2

How has the Covid-19 pandemic affected personal (household) savings? There is a trade-off between current liquidity and locking money away in assets. In our last CEDA-CMIE Bulletin we took a longer look at how intention to save has changed from January 2017 to April 2021, instead of zooming in narrowly around the pandemic. We based our analysis on CMIE data on households’ intention to save.

In Part 1, we focused on intention to save in gold, real estate, and business. We saw that there was a downturn in intention to save that started in 2017 but was made worse by the pandemic. In this part, we examine life insurance, provident fund, fixed deposits, mutual funds, and listed shares as instruments for a household to invest its savings in.

CMIE provides us the percentage of surveyed households who intend to save in a particular instrument (or avenue) for example gold or real estate or fixed deposits, in the next 120 days from the date of survey. The CMIE data provides these percentages for all households as well as broken down by slabs of annual household incomes.

As in part 1, here too we show year on year changes on a quarterly basis as the CMIE data is nationally representative on a quarterly basis.

When we look at data for all five instruments, we find a broad decline in intention to save in life insurance, and fixed deposits. There has been a sharp decline in the popularity of fixed deposits since Apr-Jun 2018 while life insurance has seen a decline after the Covid-19 pandemic hit India (Jan-Mar 2020).

We also see an increase in the popularity of provident fund to save among all income groups while mutual funds, and listed shares have maintained a consistent level of interest between Jan-Mar 2017 and Apr 2021.

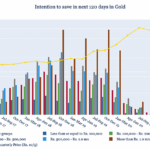

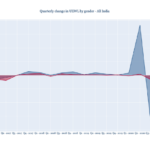

Life Insurance

Figure 1 depicts the intention to save in life insurance over the next 120 days for all income groups and all quarters starting Jan-Mar 2017. We see a similar pattern in the increase and decrease in the popularity of life insurance as an investment avenue across all income groups over this period (Jan-Mar 2017 to Apr 2021). Life insurance hit the peak of popularity in Jul-Sep 2018 (for all income groups) and has seen a steady decline since then. The sharpest decline in intention to save in life insurance is seen in Apr-Jun 2020, the first quarter after India was hit by the Covid-19 pandemic. It recovered slightly in the two following quarters and then declined again after Jan-Mar 2021 when India was hit by the second wave of the pandemic. The decline in intention to save in life insurance could perhaps be attributed to reduction in household earnings because of the Covid pandemic.

Figure 1

Mutual Funds

In Figure 2, we plot the intention to invest in mutual funds by all income groups. For all income groups combined, mutual funds hit the peak of their popularity as a saving avenue in Jan-Mar 2020. This could be attributed to the sharp increase in interest in this category for those households earning more than INR 1 million per annum. Mutual funds became more and more popular for this income group between Jul-Sep 2017 and Jan-Mar 2020.

Figure 2

Listed Shares

In Figure 3, we plot the intention to save in listed shares for all income groups between Jan-Mar 2017 and Apr 2021. The story of listed shares popularity echoes that of mutual funds. They remain of interest largely to those households earning between INR 500,000 to a million or more per annum. For the households with income more than INR 1 million per annum, listed shares see a rise in popularity till Jan-Mar 2020 (just like mutual funds) and then see a dip after the first wave of Covid-19, and another dip after the second wave of the pandemic.

As we noted in part 1 of this two-part series, high net worth individuals are under-represented in all household surveys, everywhere in the world. It is because of the difficulty in getting the super-rich to answer survey questions. CMIE data has some representation of households earning more than INR 1 million per annum.

Figure 3

Fixed Deposits

In Figure 4, we look at fixed deposits as an investment avenue for responding households. Fixed deposits display an interesting trend in their popularity in this period (Jan-Mar 2017 to Apr 2021). While we see a general weakening of their popularity over this period, it is the reverse for the highest income group (households earning more than INR 1 million per annum). For all income groups combined, fixed deposits saw peak popularity as an investment avenue in Jan-Mar 2018 while for households earning more than INR 1 million per annum, the peak of popularity was seen in Oct-Dec 2018. Fixed deposits have remained relatively more popular since then for this income group even as its wider popularity has gone down substantially.

The decline in popularity of fixed deposits could be attributed to the low interest rate regime of the RBI. With banks like SBI, and HDFC offering interest rates of only 4 to 6 percent on FDs, they have become less popular as an investment avenue.

Figure 4

Provident Fund

Figure 5 plots the intention to save in provident fund for all income groups. Unlike other saving/investment avenues, provident fund remains consistently popular. We observe that this is especially true for lower income households in the CMIE data. For the higher income groups (INR 500,000 to a million or more than INR 1 million per annum), provident fund has become more popular as a saving avenue in this period.

The consistent popularity of PF could be attributed to its linkage with salaries (owing to job regulations). As contribution to PF is defined by regulation, it makes it harder to shift out of a provident fund plan.

Figure 5

We have seen two dips in intention to save in all the savings instruments included in this bulletin. We observe the first sharp dip when India saw the first wave of Covid-19 pandemic, followed by a brief recovery, and then another sharp dip in the first quarter of 2021 when India was hit by the second wave of the pandemic.

In part 1, we had observed that the downward trend in intention to save started before the Covid-19 pandemic but has been worsened by it. But here we note that unlike other saving instruments, for equity market linked instruments (listed shares or mutual funds), the intention to save has been growing over time in the pre-pandemic period. This is especially true for high income households. From the starting point of Jan-Mar 2017, we see a significantly higher share of households intend to invest in mutual funds, and listed shares in Apr 2021. This could partly be explained by rich households’ greater tolerance for risk, or it could also be attributed to the performance of the equity markets in this period (Jan-Mar 2017 to Apr 2021). The S&P BSE Sensex has gone from 26,366 (closing on January 31, 2017) to 48,782 (closing, April 31, 2021). The keen interest shown by Foreign Institutional Investors (FIIs) in the Indian market is credited as the reason for this stock market rally in India. India saw FII inflows of $37.6 billion in 2020-21, the highest among emerging markets. The pandemic has also seen a rise in first time investors in the Indian stock markets which has driven them upwards.

According to some experts, markets have been driven up by these 14.2 million new investors in 2020-21. They now account for 45 percent of trading turnover in the NSE.

Conclusion

With a higher tolerance for taking risk, and more funds to invest, richer households have enjoyed significantly higher returns from mutual funds, and listed shares (as compared to other saving instruments). With the pandemic putting restrictions on luxury spending (vacations, dining out, going out to watch a movie, buying a new vehicle or buying new clothes/shoes etc.), these rich households would also have more funds left to invest (as luxury expenditure is constrained). Thus, richer households investing more in listed shares or mutual funds can contribute to increasing inequality in the country and the pandemic can exacerbate it.

If you wish to republish this article or use an extract or chart, please read CEDA’s republishing guidelines.

Related posts

Gold, real-estate or business: How do households intend to save?

Gold, real-estate or business: How do households intend to save?

CEDA-CMIE Bulletin no. 10: More farmers and fewer wage labourers

CEDA-CMIE Bulletin no. 10: More farmers and fewer wage labourers

CEDA-CMIE Bulletin: Manufacturing employment halves in 5 years

CEDA-CMIE Bulletin: Manufacturing employment halves in 5 years

CEDA-CMIE: In 5 years, youth employment reduces by 30 percent

CEDA-CMIE: In 5 years, youth employment reduces by 30 percent

CEDA-CMIE: India’s shrinking female workforce

CEDA-CMIE: India’s shrinking female workforce