Industrial Production: Covid only made a bad situation worse

24 May 2021 | Covid, Economic Growth, Economy, Industrial Production, Manufacturing

On May 12, 2021, the Ministry of Statistics and Programme Implementation (MoSPI), Government of India released the quick estimates of India’s Index of Industrial Production (IIP) for the month of March 2021. IIP was up 22.4 percent in March 2021, according to the release. The release also had the final numbers for the month of December 2020.

These quick estimates of IIP for a month are released on the 12th of every month with a six week lag. The final, revised numbers for March 2021, will likely be released in the month of August 2021.

Index of Industrial Production

“The all India IIP is a composite indicator that measures the short-term changes in the volume of production of a basket of industrial products during a given period with respect to that in a chosen base period. It is compiled and published monthly by the Central Statistics Office (CSO) with a time lag of six weeks from the reference month.” [1]

IIP is one of the core set of economic statistics and informs us about the level of industrial activity in the economy on a monthly basis. It provides crucial inputs for policy makers, policy analysts, industry, and financial intermediaries.

IIP has a base period of 2011-12. What this means is that activity in the year 2011-12 is considered to be 100. Figure 1 tracks IIP’s journey from April 2012 to March 2021.

Figure 1

Figure 1 also includes monthly IIP growth rate figures. IIP growth rate in a month is the percent change in Index of Industrial Production in a month relative to the same month in the previous year. Thus an IIP growth rate of 22.4 percent in March 2021 means IIP grew by 22.4 percent over IIP in March 2020. This highlights the importance of the base on which this change is recorded. IIP dipped by 18.2 percent in March 2020 to 117.2. And this low base has resulted in a sharp increase in March 2021.

Reading IIP data

IIP data can be read in two ways: looking at sectoral composition or through use-based classification.

Sectoral composition

The entire industry is composed of three sectors: mining, manufacturing and electricity. Mining carries a weight of 14.37, manufacturing carries a weight of 77.63, and electricity carries a weight of 7.99. Together these three account for IIP.

“Weights at the sectoral level for the new series of IIP have been computed using the sectoral Gross Value Added (GVA) figures from National Accounts Statistics with base 2011-12.” [2]

These sectoral weights are then further distributed at product level based on output figures from Annual Survey of Industries (ASI) 2011-12. Finally at the item level, these weights are distributed on the basis of Gross Value of Output (GVO).

Manufacturing’s 77.63 percent weight is made up of 23 sub-sectors, each carrying its own weight. For example, the manufacture of basic metals has a weight of 12.8 while manufacture of chemicals and chemical products carries a weight of 7.87.

IIP tracks indices for each of these sectors and their monthly growth rates as well. A closer look at manufacturing sub-sectors can inform the reader which particular sectors may be doing better than others.

Use-based classification

The second way to read IIP data is to look at use-based classification (UBC). In UBC, industries are divided into six categories, viz. primary goods (weight: 34.05), capital goods (w: 8.22), intermediary goods (w: 17.22), infrastructure and construction goods (w: 12.34), consumer durables (w: 12.84), and consumer non-durables (w: 15.33).

IIP data provides monthly indices, and growth rate for all six categories as well.

Sectoral growth rate

In Figure 2, we take a closer look at annual growth rates of 8 sub-sectors, combined into 6 parts. These are Manufacture of 1 (food products), 2 (textiles + wearing apparels), 3 (paper and paper products + printing and reproduction of recorded media), 4 (electrical equipment), 5 (machinery and equipment), and 6 (motor vehicles, trailers and semi-trailers). Food products, textiles, and vehicles have been chosen as they represent major consumer items in the IIP; paper and printing have been considered because of the transition to online or e-education which may have affected their demand. and electrical machinery or equipment has been chosen as the pandemic may have led to an increase in demand for electronics. These are industries which may have been most affected by the coronavirus pandemic. We look at data between 2013-14 and 2020-21.

These 8 sub-sectors (combined into 6 parts), carry a total weight of 24.09 in IIP and make up for 31 percent of total manufacturing. All 6 registered a decline in industrial activity in 2020-21. While 2 declined by 24.5 percent, 3 fell by 25.4 percent. Motor vehicles (6) saw sharp decline in industrial activity as well and fell by 19.1 percent.

However, the year 2020-21 can be considered an aberration in industrial production owing to the Covid-19 pandemic. India saw national and regional lockdowns over a considerable period of time in 2020-21 which led to such sharp decline in manufacturing which saw overall activity decline by 9.8 percent.

While the decline in 2020-21 can be explained away by the Covid pandemic and be considered an aberration, the decline in 2019-20 is harder to brush-off as an abnormality. Out of these six series, five show a decline even in the year preceding the pandemic. Except food products which saw industrial activity growing by 2 percent in 2019-20, all other sub-sectors saw a decline with motor vehicles (6) suffering the sharpest dip (18.3 percent). Overall, manufacturing declined by 1.4 percent in 2019-20 while IIP saw a decline of 0.8 percent.

This shows that Covid pandemic in 2020-21 only worsened an already deteriorating industrial situation in India.

Figure 2

Use-based classification growth rate

For the purpose of easier analysis, we have divided use-based classification of industrial activity in two parts. Figure 3 covers the first part and tracks annual growth rates for primary goods, capital goods, intermediary goods, and infrastructure/construction goods.

While 2020-21, saw a sharp decline in all categories, 2019-20 saw a sharp decline of 13.9 percent in industrial activity for capital goods. Capital goods include plant, machinery and goods used as inputs in further manufacturing. Decline in their production thus points to decline in investment in setting up new plants, and factories.

Intermediate goods (products used as inputs in further production like cotton yarn, plywood, steel tubes etc) saw 9.1 percent growth in activity in 2019-20.

Infrastructure/construction goods (finished goods used as inputs in construction or infrastructure industries) saw a decline of 3.6 percent in 2019-20.

Even primary goods, which carry the highest weight (34.05) in UBC, saw their indices of industrial production go up by only 0.7 percent in 2019-20. The downward trend in primary goods from 2015-16 to 2020-21 is an indicator of an overall slowdown in production and output.

Figure 3

Figure 4 tracks annual growth rates for consumer durables and consumer non-durables. Consumer durables includes products directly used by consumers which last for a longer period of time, like air-conditioner, television, passenger cars, telephones etc. Consumer non-durables include products which have a short shelf-life like biscuits, rice, sugar, tea, edible oil etc.

Both consumer durables and consumer non-durables saw a decline in growth rate of indices in 2019-20. Consumer durables saw a sharp dip of 8.7 percent while consumer non-durables saw a dip of 0.1 percent. The decline in industrial activity for consumer durables even in 2019-20 can plausibly be attributed to a decline in demand and an economic slowdown in the period.

This decline in both categories in 2019-20 was then followed by a sharp, Covid-induced dip in the year 2020-21, thereby exacerbating an already precarious situation.

Figure 4

Conclusion: Covid only made a bad situation worse

The IIP data released by MoSPI carries a note that says, “It may not be appropriate to compare the IIP in the post pandemic months with the IIP for months preceding the Covid 2019 pandemic.”

When we look at IIP numbers for 2020-21, the impact of the Covid-19 pandemic on India’s industrial activity becomes apparent. Between April 2020 and August 2020, IIP saw an average monthly decline of 25 percent. The impact of the Covid-19 pandemic and national (or regional) lockdowns on industrial production cannot be overstated. However, a glance at industrial activity in 2019-20 informs us of a deepening slowdown even before the pandemic struck India.

India’s economic slowdown in 2019-20 had been recognised as an extraordinary slowdown the same year. In an interview in December 2019, former Chief Economic Advisor to the PM and Professor of Economics at Ashoka University, Arvind Subramanian remarked that it was the kind of economic downturn that India hadn’t seen in 30 years.

“Electricity generation figures suggest an even grimmer diagnosis: growth is feeble, worse than it was in 1991 or indeed at any other point in the past three decades. Clearly, this is not an ordinary slowdown. It is India’s Great Slowdown, where the economy seems headed for the intensive care unit. [3]

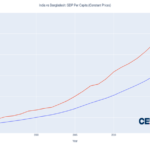

The extraordinary downturn is best captured by the slowdown in electricity generation in India in 2019-20. Figure 5 shows the rate of growth of electricity generation in India between 2012-13 and 2020-21.

Figure 5

The slowing growth in electricity generation can be taken as proxy for a wider economic downturn in India in 2019-20. Thus, Covid-19 only made a bad economy worse in 2020-21.

[1] P1, IIP 2011-12 – An Overview, MoSPI, 2018

[2] P8, IIP 2011-12 – An Overview, MoSPI, 2018

[3] P4, India’s Great Slowdown: What Happened? What’s the Way Out?, Arvind Subramanian and Josh Felman

If you wish to republish this article or use an extract or chart, please read CEDA’s republishing guidelines.