Tur-nomics: Prices of India’s favourite dal heat up

Retail prices of Tur (Arhar) dal jumped from INR 110.5 per kg on average across the country at the beginning of the year to INR 135.7 per kg by July 31, 2023. Prices of this dal have risen faster than the overall food prices.

Key highlights

- Tur (Arhar) is the most consumed among all dals by Indian households

- The dal’s prices have shot up in recent months, with the southern region seeing the highest prices and jump

- India is the largest producer of Tur (Arhar) in the world. Unseasonal rains and crop disease have led to supply shortages this year, pushing the government to import higher amounts of dal this year

- With less-than-normal rainfall in key cultivating areas, sowing of the crop this kharif season is trailing

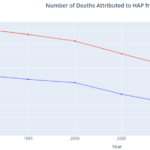

Even as the sharp surge in tomato prices in recent weeks has caught everybody’s attention, another essential kitchen staple – Tur (also called Arhar) dal – has been seeing a steady jump in prices in recent months in India. From costing INR 110.5 per kg on average across the country to consumers at the beginning of the year, the retail price of this lentil had jumped to INR 135.7 per kg by July 31, 2023, a jump of almost 23 percent in seven months. Wholesale prices too jumped by a similar proportion (22.6 percent), going from INR 101.3 per kg on January 01, 2023 to INR 124.2 per kg by July 31, 2023. (Figure 1a). A similar spike has not been observed in the price of other pulses (Figure 1b).

As is common with food prices, these jumps have been uneven in different parts of the country (Figure 2). As of July 31, 2023, the retail price of Tur varied from INR 132.3 per kg on average in the north-eastern region of the country to INR 148.9 in the southern region. The southern region also saw the highest rise in prices since a year ago. Retail prices of the dal jumped by nearly 36 percent compared to their prices a year ago (as on Aug 01, 2022). The jump was the lowest (17.8 percent) in the north-eastern region.

Tur/Arhar is among the most commonly consumed dal in India (Figure 3). Six in ten rural households (59.6 percent) and 74.1 percent urban households reported consuming Arhar dal in the preceding month in 2011-12, data from the Household Consumer Expenditure Survey (NSS Round 68) shows. On average, a rural household consumed 0.212 kg of this dal in a month while an urban household consumed 0.301 kg of this dal each month in 2011-12. In fact, Arhar accounted for as much as 27 percent of pulse consumption in rural areas and 33 percent in urban areas, the survey had observed.

Given its wide popularity in Indian kitchens, this dal carries a weight of 0.796 percent in the calculation of India’s consumer inflation, putting it behind only milk, rice, wheat, fish/prawns, chicken, sugar, potatoes and tea among individual food items. After remaining below the inflation in the combined food price index (CFPI) since Nov 2021, Arhar’s retail inflation rate surpassed the CFPI inflation in Nov 2022, and has been rising steadily ever since, data from the Ministry of Statistics and Programme Implementation (MoSPI) shows.

It’s no surprise that the price rise is beginning to pinch. A survey of 14,000 respondents conducted by a polling agency, LocalCircles, in Jun 2023 found that over a quarter of respondents had reduced their consumption of Arhar dal in recent days, and 5 percent had paused their consumption.

While the prices of Tur (Arhar) have also shot up in the past, these do not necessarily follow a seasonal trend (see Figure 5).

Supply shortages, often caused due to extreme or erratic weather events (see examples here and here), have led to sharp surges in the price of the pulse. This year too, a shortage in the availability of the dal in recent months seems to be driving the jump in prices.

India is the largest producer of Arhar in the world, and produces a dominant share of its total stockpile. Over 43 lakh tonnes of Arhar was domestically produced in India in FY 2020-21. This was 16.9 percent of all pulses that were domestically grown in the same year, data from the government’s Directorate of Pulses Development shows.

Over 96 percent of the domestic production comes from the nine states of Maharashtra, Karnataka, Madhya Pradesh, Uttar Pradesh, Gujarat, Telangana, Jharkhand, Odisha and Andhra Pradesh. In January this year, rains and wilt disease damaged Tur crops in Karnataka, paving the way for a supply shortage of the dal. Maharashtra saw unseasonal rains in April that too left behind damaged crops, which included Arhar as well. In FY 2020-21, Maharashtra and Karnataka had contributed over 28.4 percent and 24 percent of tur to the national pool respectively.

A supply crunch was in the offing. India imports about 10 percent of its stockpile from other countries. In FY 2021-22, 4.43 lakh tonnes of Arhar dal were imported, primarily from Tanzania (36 percent), Mozambique (35 percent), Myanmar (20 percent), Sudan and Uganda (2 percent each). As supplies started tightening, Indian traders were hoarding stocks of Tur they had imported from Myanmar, a report in the publication Mint highlighted. The government had to impose stock limits to check the practice. It also reached out to its neighbour to push for smooth supply of the dal.

In an attempt to boost supply and cool down prices the Indian government is set to import almost 12 lakh tonnes of the dal this fiscal, much higher than what the country usually imports (India imported 4.43 lakh tonnes of Tur in 2020-21, data from the Directorate of Pulses Development shows). This is in addition to other measures it has been taking – from removing the procurement ceiling of 40 percent for Tur and other pulses to releasing 50,000 tonnes of the dal from its buffer stock. In 2021, the government had put Tur, Moong and Urad dals in the “free” category for imports i.e. there are no limits to how much of these dals can be imported. This provision for Tur and Urad was subsequently extended multiple times and is currently applicable till March 2024.

But the clouds continue to loom over India’s much-loved dal. Only 31.51 lakh hectares of area had been sown under the crop this year as of July 28, lower than the 37.50 lakh hectare that had been sown at the same time last year, data from the Department of Agriculture and Farmers’ Welfare shows. This is owing to lower rainfall in the main cultivating regions. It could mean that stocks of the dal may not fill to the brim very soon.

Readers can explore trends in the price of Tur (Arhar) Dal and other essential commodities on CEDA’s Daily Food Price dataset.

If you wish to republish this article or use an extract or chart, please read CEDA’s republishing guidelines.